52 currency accounts. Accounting for currency transactions

Operations of enterprises on the movement of non-cash funds in foreign currencies are systematized by account 52 “Currency accounts”. It opens in banking structures operating in Russia and in other countries. The basis for the formation of turnovers and balances on foreign currency accounts are statements of servicing financial institutions with a set of attached monetary settlement documentation. The regulatory function is assigned to PBU 3/2006. In accordance with the accounting standards, the reflection of the assets of enterprises in the form of foreign currency occurs only in the ruble equivalent.

Chart of accounts: 52 accounts

Recalculation of foreign currency into rubles is carried out at the rate of the Central Bank, which was in effect on the day of the transaction with foreign exchange resources. Account 52 in accounting must be revalued in ruble terms as of each reporting date when generating financial statements.

For foreign currency accounts, enterprises can use sub-accounts:

- For foreign currency accounts opened in the territory of Russia - 52.1.

- For currency accounts in foreign banks - 52.2.

Analytics is conducted in the context of all accounts intended for keeping company funds in foreign currencies.

In the course of the organization's activities, the assessment of the currency in ruble terms may change due to fluctuations in the exchange rate. As a result, exchange differences arise, which can be positive or negative. In the first case, the tax base increases when calculating income tax, in the second case it decreases.

Postings on account 52 "Currency accounts"

When an enterprise purchases foreign currency, a combination of postings is used:

- D57 - K51, which is formed at the time of transfer of ruble funds to the bank for their exchange for foreign currency;

- D52 - K57 - correspondence created after the completion of a currency exchange transaction and crediting funds to a foreign currency account.

When selling foreign currency, the following records are made:

- D57 - K52 - when transferring money from a foreign currency account for exchange;

- D51 - K57 - the currency exchange is made, the proceeds are credited to the current ruble account.

Account 52 in accounting, when debiting funds, generates postings with debit accounts:

- 60 when paying in foreign currency to the supplier;

- 66, 67 on transactions for the return of borrowed funds and interest on them;

- 75, 79, 76 for transfers in favor of other counterparties.

Debit turnovers on account 52 are in correspondence with the credit of accounts:

- 62 upon receipt of payment from buyers;

- 66, 67 when receiving a loan in foreign currency;

- 75, 76, 79 when crediting funds from other counterparties.

Account 52: accounting by example

LLC "Info" sells 300 Brazilian reais from a foreign currency account. The transaction date is 07/10/17, the Central Bank exchange rate for the Brazilian real on that day is 18.3039 rubles, the bank rate is 18.3030 rubles, the bank commission is 180 rubles.

In accounting, postings are formed:

- D57 - K52 - funds in foreign currency were allocated for sale in the amount of 5491.17 rubles. (300 reais x 18.3039).

- D51 - K91.1 - the bank made the exchange and credited the enterprise with the proceeds from the sale of foreign currency in the amount of 5490.90 rubles. (300 x 18.3030).

- D91.2 - K51 for 180 rubles. when paying bank fees.

- D91.2 - K57 to reflect the formed negative exchange rate difference of 0.27 rubles. ((18.3039-18.3030) x 300).

- D91.2 - K57 at the time of writing off foreign currency in the amount of 5491.17 rubles.

In this article, we will analyze how accounting for operations on a foreign currency account how the purchase and sale of currency takes place, what are exchange rate differences, and how they are taken into account in the accounting department of the enterprise. Account 52 “Currency accounts” is used to account for currency. In this article, we will analyze what transactions are reflected in the currency account and how to take them into account, what key transactions, sub-accounts and offsetting accounts exist.

Accounting for foreign currency has some features associated with the fact that in Russia it is carried out in monetary units - rubles. In this connection, it becomes necessary to take into account foreign currency also in rubles. To account for transactions on 52, the rate of the Central Bank of Russia is taken.

The purchase and sale of foreign currency is carried out only through banks, and not all banks can buy and sell currency, only those that have permission to do so.

Organizations carrying out export-import operations open a foreign currency account in a bank. If several types of currency are used, then, as a rule, more than one account is opened. For each type of currency - a separate currency account.

To open a foreign currency account, the organization selects a suitable bank, collects the necessary package of documents and submits them to the selected bank. The bank, in turn, opens two accounts for the organization: current and transit. All transfers in foreign currency to the address of the account holder go through the transit account. The current currency account reflects the actual amount of currency the company has.

Video lesson. Account 52 in accounting

This video tutorial describes in detail about account 52 in accounting, examples of use and documents. The lesson is conducted by the chief accountant Gandeva N.V., expert and consultant of the site Accounting for dummies ⇓

To download the presentation using the video, click on the link below.

Buying currency: postings, exchange rate differences

How is the purchase of currency?

In order to buy foreign currency, the organization transfers to the bank a certain amount of money in rubles from its ruble current account. At the same time, in accounting, this transfer is reflected in the posting D57 K51. sch. 57 "Transfers on the way" - intermediate between 51 "Settlement account" and 52 "Currency accounts". The money was debited from, but we still cannot credit it to the currency account, since the bank has not yet transferred the currency to us. To prevent this money from being lost and forgotten, an intermediate account is used. 57 "Transfers on the way".

After the organization has transferred the required amount of money to the bank in rubles, the bank purchases the required amount of foreign currency and transfers it to the enterprise's foreign currency account (the currency is taken into account converted into rubles at the exchange rate of the Central Bank of Russia effective on the date of transfer). accounting entry D52 K57.

Remaining funds in the account 57 are transferred back to the settlement account (posting D51 K57).

For carrying out a transaction for the purchase of foreign currency, the bank withholds a commission, the amount of which is attributed to an increase in the value of acquired material assets or as part of. The posting reflecting the payment of the commission looks like this: D91/2 K51, where on account 91 subaccount 2 operating expenses are taken into account.

The acquired foreign currency is accounted for at the official exchange rate of the Central Bank of Russia, effective on the date of its receipt.

At the same time, the rate used when purchasing foreign goods may differ from the official rate of the Central Bank of the Russian Federation. The resulting difference is called the financial result from the purchase of the currency.

If the official rate is less than the purchase rate, then in accounting the resulting difference is reflected as part of operating expenses. ( D91/2 K57- negative difference).

If the official rate is greater than the purchase rate, then the difference is reflected in operating income ( D57 K91/1 is a positive difference).

At the time of payment for foreign goods, the supplier must recalculate the currency at the exchange rate of the Central Bank of the Russian Federation on the date of payment:

If the exchange rate on the date of payment to the supplier is higher than that of the Central Bank of the Russian Federation on the date the currency is credited to the account. 52, then there is a positive exchange difference, which is reflected in other income by posting D57 K91/1.

If the exchange rate of the Central Bank of the Russian Federation on the date of payment is lower than on the date the currency is credited to the foreign currency account, then a negative exchange rate difference arises, which is reflected in other expenses by posting D91/2 K57.

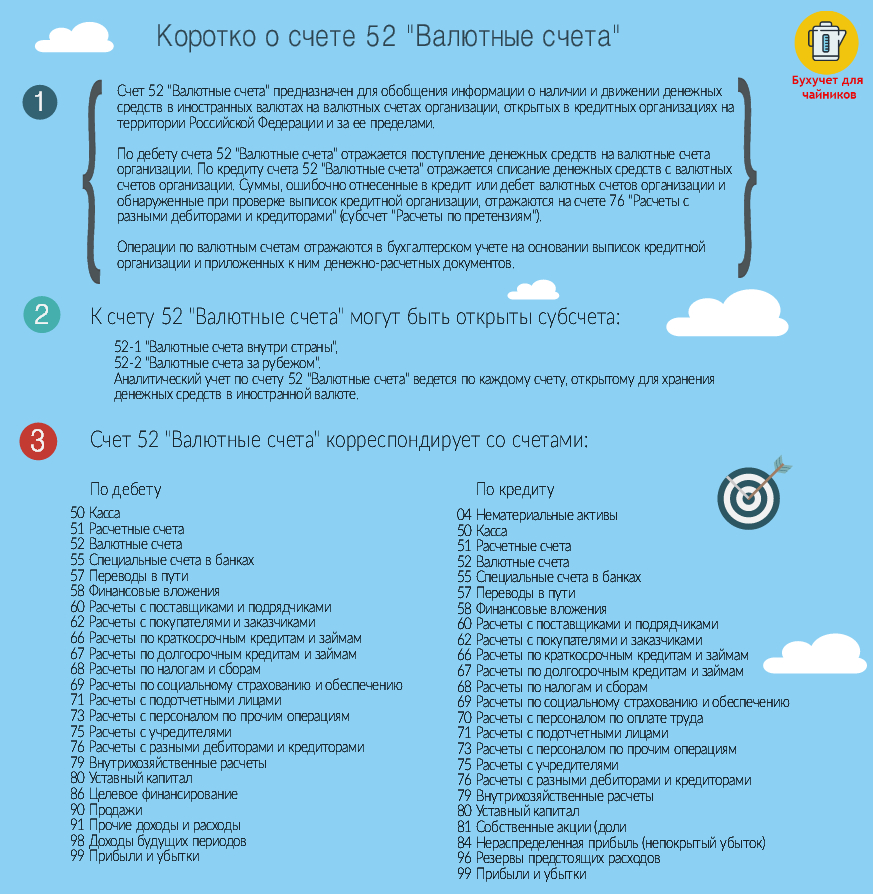

Briefly about account 52 in infographics

In the figure below, the infographic provides brief information about account 52, what sub-accounts and corresponding accounts it has. Click on the image to open in full size.

Transactions for account 52 when buying currency

Debit | Credit | Operation name |

The required amount of money was transferred to the bank in rubles (at the exchange rate of the bank) |

||

The purchased currency is credited to the currency account (at the rate of the Central Bank of Russia) |

||

The funds remaining after the purchase of the currency were returned to the current account |

||

Commission withheld |

||

A negative difference is reflected (the purchase rate is higher than the CBR) |

||

A positive exchange rate difference is reflected (the purchase rate is below the Central Bank of the Russian Federation) |

Accounting for transactions upon receipt of foreign currency from the buyer

When receiving currency from foreign buyers for goods, works, services, it is credited to the "Currency transit account", this operation is reflected in the posting D52 K62, where 62 "Settlements with buyers".

After that, it can either be sold or credited to a current foreign currency account. The currency directed to the sale is debited D57K52. Previously, part of the received foreign exchange funds had to be sold without fail, recently the mandatory sale of foreign currency has been canceled.

Accounting for transactions in the sale of foreign currency

The sales process also involves the use of account. 57, as in the case of the purchase. The currency intended for sale is transferred to the bank that sells it and credits the proceeds from the sale to the company's current account.

The transaction for transferring currency to a bank for sale looks like D57 K52.

In the accounting department, the currency was accounted for at the exchange rate of the Central Bank of Russia, effective on the date of either the last revaluation, or on the date of crediting to the account. 52. On the day of the sale, a currency translation must be carried out.

In this case, both positive (if the exchange rate of the Central Bank of the Russian Federation on the date of recalculation is higher than on the date of crediting to the account) and negative exchange rate differences can occur.

The sale of currency is processed through account 91. The value of the currency is debited to account 91 by posting D91/2 K57 at the rate of the Central Bank of the Russian Federation. The proceeds from the sale are credited to the ruble account at the selling rate, while posting D51 K91/1.

The bank sells currency at its own rate, which may differ from the Central Bank. In addition, foreign exchange funds can be transferred to the bank for sale on one day, and the bank will sell the currency on another day, and there may also be an exchange rate difference (if the exchange rate of the Central Bank of the Russian Federation has changed during this time). Negative exchange rate difference is reflected in the posting D91/2 K57, positive - D57 K91/2.

According to the results of the transaction for the sale of foreign currency on account 91, the financial result (profit or loss) is considered.

Transactions when selling currency

Debit | Credit | Operation name |

The currency intended for sale is listed (at the exchange rate of the Central Bank of the Russian Federation) |

||

Sales proceeds received (at the selling rate) |

||

The value of the currency sent for sale was written off (at the exchange rate of the Central Bank of the Russian Federation on the date of sale) |

||

A negative exchange rate difference is reflected (due to the change in the exchange rate of the Central Bank of the Russian Federation on the date of debiting from the foreign currency account and on the date of sale) |

||

Reflected a positive exchange rate difference (similarly) |

||

Financial result from the transaction loss (profit) |

Revaluation of foreign currency accounts (revaluation of account 52)

The currency is revalued periodically.

Funds on foreign currency accounts are reflected in accounting and reporting in rubles. Therefore, the currency is converted into rubles at the official exchange rate of the Central Bank of the Russian Federation, effective on the date of conversion.

Thus, the revaluation of foreign currency accounts is carried out:

- on the date of crediting or debiting currency from bank accounts;

- on the date of preparation of financial statements;

- as the course changes.

Postings for currency revaluation:

As a result of the translation, a foreign exchange difference arises, which is reflected in operating income. (D52 K91/1) and expenses (D91/2 K52).

The organization's funds can be kept not only at the cash desk, but also in bank accounts. To account for funds in foreign currency that are stored in the organization's currency accounts in the Russian Federation and abroad, the Chart of Accounts and Instructions for its use provide for an active account 52 "Currency accounts" ().

Sub-accounts to account 52 and analytical accounting

To account 52, such sub-accounts are usually opened (Order of the Ministry of Finance dated October 31, 2000 No. 94n):

- 52-1 "Currency accounts within the country";

- 52-2 "Currency accounts abroad".

Analytical accounting on account 52 is maintained for each account that was opened to store money in foreign currency.

Accounting on account 52

Based on the bank statements and the monetary settlement documents attached to them, entries are formed on account 52. Since account 52 is active, the receipt of foreign currency is reflected in the debit of this account, and the write-off is reflected in the credit.

Debit of account 52 - Credit of accounts 62 “Settlements with buyers and customers”, 60 “Settlements with suppliers and contractors”, 57 “Transfers on the way”, 66 “Settlements on short-term loans and loans”, etc.

Accordingly, the following transactions may correspond to the withdrawal of money from a foreign currency account:

Debit of accounts 60, 62, 66, 57, etc. - Credit of account 52

If funds from a foreign currency account were debited erroneously or were incorrectly credited to the organization's account, account 52 corresponds with account 76 "Settlements with various debtors and creditors", sub-account "Settlements on claims".

It can be said that accounting on a foreign currency account is generally carried out similarly to accounting on an organization's current account. But there is also a fundamental difference. Since operations on a foreign currency account are carried out in foreign currency, and accounting must be kept in rubles, foreign exchange transactions are reflected simultaneously in two dimensions: in the currency of settlements and in rubles (paragraph 20 of PBU 3/2006). At the same time, the currency amounts of receipts and withdrawals from the foreign currency account are converted into rubles at the exchange rate of the Central Bank of the Russian Federation in force on the date of the transaction (clause 5 of PBU 3/2006). In addition, currency account balances are also recalculated at the end of each month (clause 7 of PBU 3/2006). The differences arising from the recalculation of the currency account are referred to as exchange rate differences and are reflected as follows:

Debit account 52 - Credit account 91 "Other income and expenses"

Or Debit account 91 - Credit account 52

We talked about exchange rate differences in more detail in a separate one.

In the balance sheet, the ruble debit balance of account 52, recalculated at the exchange rate of the Central Bank of the Russian Federation on the reporting date, is reflected in line 1250 “Cash and cash equivalents” (

Account 52 "Currency accounts" is intended to summarize information on the availability and movement of funds in foreign currencies on the organization's foreign currency accounts opened with credit institutions in the Russian Federation and abroad.The debit of account 52 "Currency accounts" reflects the receipt of funds to the currency accounts of the organization.

The credit of account 52 "Currency accounts" reflects the write-off of funds from the organization's foreign currency accounts. The amounts erroneously credited or debited to the organization's foreign currency accounts and found when checking the statements of the credit organization are reflected on account 76 "Settlements with various debtors and creditors" (subaccount "Settlements on claims").

Operations on foreign currency accounts are reflected in the accounting records on the basis of the statements of the credit institution and the monetary settlement documents attached to them.

To account 52 "Currency accounts" sub-accounts can be opened:

52-1 "Currency accounts within the country";

52-2 "Currency accounts abroad".

Analytical accounting on account 52 "Currency accounts" is kept for each account opened for keeping funds in foreign currency.

On account 52 "Currency accounts" organizations reflect currency operations for crediting and debiting funds from foreign currency accounts.

The definition of a currency transaction is given in the Law of the Russian Federation dated October 09, 1992 No. 3615-1 “On currency regulation and currency control”. Foreign exchange transactions include:

Operations related to the transfer of ownership and other rights to currency values, including operations related to the use of foreign currency as a means of payment and payment documents in foreign currency;

Import and transfer to the Russian Federation, as well as export and transfer from the Russian Federation of currency values;

Implementation of international money transfers;

Settlements between residents and non-residents in the currency of the Russian Federation.

This definition emphasizes that when performing foreign exchange transactions, the transfer of ownership of currency values (foreign currency, securities in foreign currency, etc.) takes place. However, there are transactions that do not entail the transfer of ownership of currency values. For example, receiving foreign currency from a foreign currency account at the cash desk does not lead to the transfer of ownership of foreign currency (the organization remains its owner). Therefore, in practical work, one should proceed from the fact that foreign exchange transactions are facts of economic life associated with the movement of foreign exchange values and the adjustment of their assessment. The latter is understood as the recalculation of currency items of the balance sheet at the rate of the Central Bank of the Russian Federation on the date of preparation of the financial statements.

Accounting for foreign exchange transactions is carried out in accordance with the Accounting Regulation "Accounting for assets and liabilities of an organization, the value of which is expressed in foreign currency" (PBU 3/2000), approved by order of the Ministry of Finance of the Russian Federation dated 10.01.2000 No. 2n.

Foreign exchange transactions are accounted for in two estimates:

a) in foreign currency;

b) in rubles.

For accounting purposes, foreign currency is converted into rubles at the exchange rate quoted by the Central Bank of the Russian Federation.

The conversion of foreign currency into rubles is carried out in two cases:

1) when making a currency transaction;

2) when revaluing currency balance sheet items.

In the first case, the conversion of foreign currency into rubles is carried out by multiplying the amount of foreign currency by the exchange rate of the Central Bank of the Russian Federation on the date of the transaction.

In accordance with paragraph 75 of the Regulation on accounting and financial statements and paragraph 7 of PBU 3/2000, when compiling the balance sheet, its currency items must be revalued

sya. The list of these items is specified in the above paragraphs of the relevant regulatory documents: banknotes kept at the cash desk of the organization, funds in accounts with credit institutions, cash and payment documents, short-term securities, funds in settlements (including for loan obligations) with legal entities and individuals, balances of special-purpose financing received from the budget or foreign sources within the framework of technical or other assistance of the Russian Federation in accordance with concluded agreements (contracts), denominated in foreign currency.

The revaluation procedure consists in converting foreign currency into rubles at the exchange rate of the Central Bank of the Russian Federation as of the last day of the reporting period.

Foreign currency held in cash and on bank accounts may be revalued as foreign exchange rates change.

The value of the same assets and/or liabilities may be recalculated into rubles on different dates. Since the exchange rates quoted by the Central Bank of the Russian Federation are constantly changing, this leads to exchange rate differences.

According to paragraph 3 of PBU 3/2000, the exchange difference is understood as “the difference between the ruble valuation of the relevant asset or liability, the value of which is expressed in foreign currency, calculated at the rate of the Central Bank of the Russian Federation on the date of fulfillment of payment obligations or the reporting date of the financial statements for the reporting period, and the ruble valuation of these assets and liabilities, calculated at the rate of the Central Bank of the Russian Federation on the date of their acceptance for accounting in the reporting period or the reporting date of the preparation of financial statements for the previous reporting period. In other words, the exchange rate is the difference between the ruble valuation on different dates of assets and / or liabilities, the value of which is expressed in foreign currency.

Exchange differences can be positive or negative. Positive exchange differences increase taxable income, while negative exchange differences reduce it.

Exchange differences are reflected on account 91 “Other income and expenses”, positive - on the loan of sub-account 1 “Other

income", and negative - on the debit of sub-account 2 "Other expenses". The exception is exchange differences arising from settlements on contributions to authorized capital in foreign currency, which are reflected in account 83 “Additional capital”. It should be emphasized that the exchange rate difference associated with the formation of the authorized (reserve) capital of an organization is defined as the difference between the ruble assessment of the debt of the founder (participant) on the contribution to the authorized (reserve) capital of the organization, valued in the constituent documents in foreign currency, calculated at the exchange rate of the Central Bank of the Russian Federation on the date of receipt of the amount of deposits, and the ruble assessment of this contribution in the constituent documents.

The organization can open currency accounts either by type of currency (US dollars, British pounds sterling, etc.) or for the main foreign currency of payment (for example, US dollars). In the latter case, the bank independently converts incoming or made payments in other currencies into the main currency (for example, US dollars).

In the explanations to account 52 "Currency accounts" of the Instructions for the use of the Chart of Accounts, it is recommended to open two sub-accounts:

52-1 "Currency accounts within the country"; 52-2 "Currency accounts abroad".

We believe that in order to account for funds in foreign currency accounts within the country, several sub-accounts should be opened:

1. "Transit currency account".

2. "Special transit currency account".

3. "Current currency account".

The transit currency account is credited with export currency earnings, 50% of which is transferred to the bank for mandatory sale, and 50% - to the current currency account. The organization's foreign currency is kept in a current foreign currency account, and payments in foreign currency are made from it.

A special transit currency account is opened by an organization if it purchases foreign currency. The purchased currency is credited to this account and must be used by the organization for the purposes for which it was purchased within seven calendar days. If during this period the currency has not been used, it is subject to resale.

In its activities, the organization can:

- receive loans (credits) in foreign currency.

Accounting for currency transactions is carried out on the basis of PBU 3/2006 and the Chart of Accounts and Instructions for its application. To summarize information on the availability and movement of foreign currency on foreign currency accounts opened with authorized banks in Russia or in banks outside of it, account 52 "Currency accounts" is intended. To account 52, you can open sub-accounts - “Currency accounts within the country”, “Currency accounts abroad”. Analytical accounting for account 52 must be kept for each account opened for keeping money in foreign currency. This follows from the Instructions for the Chart of Accounts.

Purchase of currency

The organization has the right to purchase foreign currency only through an authorized bank (Article 11 of the Law of December 10, 2003 No. 173-FZ).

To purchase foreign currency, draw up a settlement document (clause 3.1 of Instructions of the Bank of Russia dated June 4, 2012 No. 138-I). The uniform form of the settlement document is not established by the legislation. As a rule, banks have the necessary forms. In the settlement document, before the text part in the "Purpose of payment" attribute, indicate the code for the type of transaction from the list of currency and other transactions (clause 3.2 of Instructions of the Bank of Russia dated June 4, 2012 No. 138-I). When buying foreign currency, indicate the currency transaction code 01 030 (Appendix 2 to Instructions of the Bank of Russia dated June 4, 2012 No. 138-I).

To purchase foreign currency for an employee's business trip, see How to reflect in accounting cashless purchase currencies for business trips .

To reflect the transaction for the purchase of currency in accounting, you can use account 57 “Transfers on the way”. This is possible if the issuance of the settlement document to the bank for the purchase of currency does not coincide with the date of its receipt in the currency account. However, if rubles are debited from the account, they are sold and the currency is credited on the same day (this can be determined from bank statements), then account 57 can not be applied.

When transferring rubles for the purchase of currency, make a transaction:

Debit 57 (76) Credit 51

- transferred money for the purchase of currency.

The receipt of the purchased currency on the current account reflect as follows:

Debit 52 Credit 57 (76)

- currency is credited to a foreign currency account (based on a bank statement).

Capitalize the received currency at the official exchange rate in force on the date the money is credited to the organization's currency account. At the same time, make entries in the accounting registers both in the currency of settlements (rubles) and the currency of payments.

This procedure follows from paragraphs 4-6, 20 PBU 3/2006, paragraph 24 of the Regulation on accounting and reporting and the Instructions for the chart of accounts (accounts 52, 57, 76).

The exchange rate at which the bank buys it usually differs from the official one. If the currency is bought more expensive than the rate of the Bank of Russia, there is another expense from the currency purchase operation (clause 11 PBU 10/99). If cheaper - other income (clause 7 PBU 9/99).

In most banks, you will have to pay a commission for the purchase of foreign currency. In accounting, include this amount in other expenses (paragraph 7, clause 11, PBU 10/99).

An example of the reflection in accounting of a transaction for the purchase of foreign currency

Alfa LLC signed a foreign trade contract. For its execution, Alfa needs US dollars. There is no money in the organization's foreign currency account. Therefore, on January 30, Alfa instructed the bank to purchase the necessary currency (1,000 US dollars). To do this, they compiled a settlement document and transferred 31,000 rubles for the purchase of foreign currency.

On February 2, the bank bought the currency at the rate of 30.50 rubles. per dollar and credited it to the organization's foreign currency account minus a commission in the amount of 200 rubles.

The accountant of the organization made the following entries in the accounting.

Debit 57 Credit 51

- 31,000 rubles. - transferred money for the purchase of currency.

Debit 52 Credit 57

- 29 700 rubles. (1000 USD × 29.70 rubles / USD) - the currency is credited to the organization's currency account;

Debit 91-2 Credit 57

- 200 rub. - commission fee is retained by the bank;

Debit 91-2 Credit 57

- 800 rubles. (1000 USD × (30.50 RUB/USD - 29.70 RUB/USD)) - reflects the difference between the currency purchase rate and the rate of the Bank of Russia;

Debit 51 Credit 57

- 300 rubles (31,000 rubles - 1000 USD × 30.50 rubles / USD - 200 rubles) - the balance of unspent money has been returned.

Accounting for foreign exchange earnings

The receipt of foreign exchange earnings from the sale of goods (performance of work, provision of services) is reflected in account 52. Sub-accounts should be opened for it:

- "Current currency account";

- "Transit currency account".

Transfer the funds received in foreign currency into rubles at the official exchange rate of the Bank of Russia, established on the date of their transfer to the organization's transit currency account (paragraph 1, clause 5, PBU 3/2006). At the same time, make an entry in the foreign currency accounting registers. This follows from paragraph 24 of the Regulation on accounting and reporting.

Accounting for the receipt of foreign exchange earnings depends on the terms of the contract. In particular, from:

- on what date the ownership of the goods is transferred or when the works (services) are considered accepted by the customer (as of the date of shipment, the date of signing the act, the date of payment, the date of execution of the customs declaration, etc.);

- whether the contract provides for an advance payment.

If ownership passes on the date of shipment (a different date than the date of payment) and the contract provides for subsequent payment, make the following entries.

Debit 62 Credit 90-1

- reflected the proceeds from the sale of goods.

On the payment date:

- reflected payment by the buyer of the goods;

This procedure follows from paragraph 12 of PBU 9/99 and the Instructions for the chart of accounts (accounts 52, 62, 90-1).

If the contract provides for an advance payment, the advance payment received is not recognized as the income of the organization and is reflected in accounts payable (clauses 3 and 12 of PBU 9/99). Reflect the receipt of foreign exchange earnings in this case as follows.

On the payment date:

- received an advance payment in foreign currency;

Debit 52 subaccount "Current currency account" Credit 52 subaccount "Transit currency account"

- the currency is transferred to the current currency account.

As of the date of transfer of ownership:

Debit 62 subaccount "Settlements for shipped goods (works, services)" Credit 90-1

- reflected the proceeds from the sale of goods (performance of work, provision of services);

Debit 62 subaccount “Settlements on advances received” Credit 62 subaccount “Settlements on shipped goods (works, services)”

- prepayment received.

Such a posting scheme follows from paragraph 12 of PBU 9/99 and the Instructions for the chart of accounts (accounts 52, 62, 68, 76, 90).

Regardless of the terms of the contract in accounting, the organization must re-evaluate the requirements (obligations) in foreign currency. But the advances issued (received), determine at the rate of the Bank of Russia on the date of transfer of the prepayment and do not reevaluate in the future (clause 10 PBU 3/2006).

Reassess on the date:

- performing an operation;

- reporting date (on the last day of each month).

In addition, in the accounting policy for accounting purposes, you can prescribe the procedure for revaluing foreign currency as the exchange rate changes.

This is provided for by paragraphs 7, 9-10 of PBU 3/2006, paragraph 7 of PBU 1/2008.

The revaluation results in exchange rate differences:

- positive - if the exchange rate against the ruble on the date of revaluation is higher than on the date of initial accounting of foreign currency;

- negative - if the exchange rate against the ruble falls.

This follows from paragraph 4 of clause 3 and clause 11 of PBU 3/2006.

It is advisable to issue the calculation of exchange rate differences in the form of an accounting statement-calculation drawn up in any form.

Take into account positive exchange differences as part of other income (clause 7 of PBU 9/99). Negative exchange differences - in other expenses (clause 11 PBU 10/99). This is also stated in paragraph 13 of PBU 3/2006.

An example of the reflection in accounting of an operation for the sale of goods for export. Settlements are made in foreign currency. The agreement provides for the transfer of ownership of the goods after crossing the border

Alfa LLC entered into a foreign trade contract for the supply of goods. Contract amount - 10,000 US dollars (VAT - 0%). According to the terms of the contract, ownership passes to the buyer after customs clearance for export.

On January 28, Alfa shipped goods for export. The cost of goods sold is 230,000 rubles. Customs clearance was completed on February 1.

The buyer paid for the goods as follows:

- transferred an advance payment in the amount of 30 percent of the contract amount - on January 26;

- paid the rest - on February 1.

- January 26 - 29.70 rubles / USD;

- January 31 - 29.90 rubles / USD;

- February 1 - 29.80 rubles / USD.

To reflect the operation in accounting, the accountant opened:

- to account 62 "Settlements with buyers and customers" - sub-accounts "Settlements on advances received" and "Settlements on shipped goods";

- to account 52 "Currency accounts" - sub-accounts "Current currency account" and "Transit currency account".

Debit 52 subaccount "Transit currency account" Credit 62 subaccount "Calculations on advances received"

- 89 100 rubles. (USD 3,000 × 29.70 RUB/USD) - a partial prepayment has been received from a foreign organization against the forthcoming delivery of goods;

Debit 52 subaccount "Current currency account" Credit 52 subaccount "Transit currency account"

- the currency is transferred to the current currency account.

Debit 45 Credit 41

- 230,000 rubles. - Shipped goods for export.

Debit 52 subaccount "Current currency account" Credit 91-1

- 600 rubles (3000 USD × (29.90 RUB/USD - 29.70 RUB/USD)) - reflects a positive exchange rate difference on funds in a foreign currency account.

Debit 91-1 Credit 52 subaccount "Current currency account"

- 300 rubles (USD 3,000 × (RUB 29.90/USD - RUB 29.80/USD)) reflects the negative exchange rate difference on funds in the foreign currency account;

Debit 62 subaccount "Settlements for shipped goods" Credit 90-1

- 297,700 rubles. (89,100 rubles + (10,000 USD - 3,000 USD) × 29.80 rubles / USD) - revenue from the sale of goods is reflected;

Debit 90-2 Credit 45

- 230,000 rubles. - written off the cost of goods sold;

Debit 62 subaccount "Calculations on advances received" Credit 62 subaccount "Calculations on shipped goods"

- 89 100 rubles. - advance payment made.

Debit 52 subaccount "Transit currency account" Credit 62 subaccount "Settlements for shipped goods"

- 208 600 rubles. ((10,000 USD - 3,000 USD) × 29.80 RUB/USD) - the debt on payment for the shipped goods has been repaid;

Debit 52 subaccount "Current currency account" Credit 52 subaccount "Transit currency account"

- the currency is transferred to the current currency account.

To calculate exchange rate differences on funds in a foreign currency account, the accountant issued certificates for January 31 and February 1.

An example of the reflection in accounting of an operation for the sale of goods for export. Settlements are made in foreign currency. The contract provides for the transfer of ownership of the goods after shipment. Payment is made after shipment

Alfa LLC entered into a foreign trade contract for the supply of goods. Contract amount - 10,000 US dollars (VAT - 0%). According to the terms of the contract, ownership passes to the buyer after shipment.

On January 28, Alfa shipped goods for export. The cost of goods sold is 230,000 rubles. On February 1, the buyer will pay for the goods in full.

The US dollar exchange rate set by the Central Bank of the Russian Federation was (conditionally):

- from January 26 - 29.70 rubles / USD;

- from January 29 - 29.90 rubles / USD;

- from February 1 - 29.80 rubles / USD.

The following entries were made in accounting.

Debit 62 Credit 90-1

- 297,000 rubles. (USD 10,000 × 29.70 RUB/USD) - revenue from the sale of goods after their shipment is reflected;

Debit 90-2 Credit 41

- 230,000 rubles. - written off the cost of goods sold.

Debit 62 Credit 91-1

- 2000 rub. (USD 10,000 × (RUB 29.90/USD - RUB 29.70/USD)) - reflects a positive exchange rate difference on the buyer's obligation arising from a change in the exchange rate on the reporting date.

Debit 52 subaccount "Transit currency account" Credit 62

- 298,000 rubles. (10,000 USD × 29.80 RUB/USD) - payment for the shipped goods has been received;

Debit 52 subaccount "Current currency account" Credit 52 subaccount "Transit currency account"

- the currency is transferred to the current currency account.

Debit 91-1 Credit 62

- 1000 rubles. (USD 10,000 × (RUB 29.90/USD - RUB 29.80/USD)) - reflects a negative exchange rate difference on the buyer's obligation arising from a change in the exchange rate on the date of payment.