Benefits according to IIS. Tax deduction for an individual investment account

This year, for the first time, Russians who have opened an individual investment account can apply for a tax deduction on contributions to an individual investment account for the previous calendar year. To do this, account holders must submit the necessary documents to the tax office from January 1 to April 30. To help private investors who wish to return the treasured 13% discount this year, FinancialOne has prepared brief instructions for filing a tax deduction.

First of all, let us remind you that the owner of an IIS has two ways to take advantage of the tax benefits provided for by law. The first implies that a private investor will issue a tax deduction at the end of the calendar year in which he made a contribution to his investment account. The profitability of IIS operations is not taken into account. That is, if in December 2015 a Russian opened an IIS and deposited 400 thousand rubles into it, then already in January of this year he has the right to submit the relevant documents to the tax office and get back 13% of this amount - 52 thousand rubles.

A private investor can repeat this procedure annually, but a prerequisite is the availability of income in the year for which it is planned to receive the deduction. Thus, the funds that will be returned to the IIS owner from the budget cannot exceed the amount of personal income tax paid by him during the year in which the account was opened.

A private investor will be able to use the second method of obtaining benefits only three years after concluding an agreement for maintaining an individual investment account. In this case, the account owner simply will not have to pay personal income tax on the investment profit received during this period. It does not matter whether the private investor had other sources of income taxed at a rate of 13%. Since this type of benefit is not yet available to Russians (IIS appeared on the market in 2015), it makes sense to consider in detail only the tax deduction of the first type.

REQUIRED DOCUMENTS

So, if there are withheld taxes, and therefore a source of income in 2015, the owner of the IIS needs to take the following steps to apply for a tax benefit:

– obtain from the broker or management company documents confirming the transfer of the contribution to the IIS;

– obtain form 2-NDFL from the employer;

– fill out the 3-NDFL declaration;

– write a tax refund application;

– submit documents to the tax service at the place of permanent registration.

STEP 1: PROVE THAT THERE ARE FUNDS IN THE IIS

The first point in this simple manual is to obtain documents confirming the transfer of funds to the IIS. These include, first of all, a copy of the agreement on opening an investment account, a payment order for the transfer of funds and a receipt for the transaction. “We provide clients with the following papers: General agreement and application for Comprehensive Services (a document confirming the fact of opening an IIS), as well as payment documents confirming the crediting of funds to the IIS (receipt, payment order for the payment of funds),” Igor told Financial One Sobolev, head of integrated financial solutions at FG BCS.

It should be noted that the set of documents that different brokerage companies provide for filing a tax deduction may vary slightly. Thus, IH Finam, among other things, issues to its clients who have opened an IIS, Form 2-NDFL and a broker’s report for the previous tax period.

Obtaining Form 2-NDFL from the employer or organization that provided the income of the IIS owner in 2015 is a fairly simple procedure. According to the Labor Code of the Russian Federation, the employer must issue it no later than three working days from the date of submission of the employee’s application. The title of form 2-NDFL must indicate the year for which it was issued, and the certificate itself must contain information about the employer (name, details); employee data; income taxed at the base 13% rate – monthly; standard, social and property tax deductions with codes; The total amount of income, deductions, and taxes withheld. It is extremely important that form 2-NDFL is completed correctly, since tax authorities, as a rule, scrupulously check this document.

STEP 3: COMPLETE THE DECLARATION

The most difficult part in the deduction procedure is filling out the declaration in Form 3-NDFL. It can be easily found on the Internet - for example, on the website of the Federal Tax Service. Data on the investment tax deduction in the amount of the contribution to the IIS are indicated in paragraph 3 of sheet E2 (“Calculation of investment tax deductions”). A private investor needs to register income and expenses from operations using an individual investment account, as well as the amount of tax withheld and transferred to the budget based on the 2-NDFL certificate. By the way, the instructions for filling out the declaration, which is attached to form 3-NDFL, have been supplemented with clause 13.4, which explains what needs to be written in clause 3.

Sheet E2 in certificate 3-NDFL for 2015

The good news is that brokerage companies are meeting the needs of clients who own personal investment accounts, helping them with the preparation and filing of tax returns. For example, IH Finam plans to launch a new online service in the near future, which will allow private investors not only to fill out 3-NDFL electronically using the so-called electronic signature, but also to submit a declaration to the Federal Tax Service via the Internet. This service is currently in the testing stage.

FG BCS plans to launch a similar service. It will be available to the company’s clients in the BCS Online Personal Account and will allow them to receive a completed Form 3-NDFL for submission to the tax authority without unnecessary hassle. “In the future, focusing on customer demand and wishes, we intend to expand remote support services so that IIS owners can process tax deductions as competently as possible, as well as other tax benefits,” added Igor Sobolev, head of integrated financial solutions at FG BCS.

The Otkritie Broker company, in turn, will provide consulting support to its clients applying for tax deductions under IIS. In addition, private investors who have opened an individual investment account with this brokerage company have the opportunity to submit a declaration electronically through the government services portal. Gleb Titov, head of the investment products department at Otkritie Broker, noted in a conversation with Financial One that the procedure for processing tax deductions under IIS has not yet been tested in the tax service itself, so filing a declaration electronically is the preferred option. “One of our clients, having come with a package of documents to the tax office at the place of registration, was faced with a complete misunderstanding: as it turned out, the service employees were not aware of what an IIS is and what deduction can be obtained from it. They even had to call their superiors at the Federal Tax Service,” the financier explained.

STEP 4: SUBMIT DOCUMENTS

When filing a tax return, the IIS owner must also attach a tax refund application indicating bank details. A private investor can obtain a sample of this statement from the tax office or from his broker. There are four ways to submit Form 3-NDFL:

– in electronic form through the website of the Federal Tax Service of Russia (using the “Taxpayer Personal Account” service), signing it with a non-qualified electronic signature, which can be generated on the same resource;

– in electronic form via telecommunication channels, using the taxpayer’s enhanced electronic signature, which will need to be obtained from a certification center;

–by mail with a description of the attachment;

– in person to the tax office in paper form.

When filing a return online, a private investor will need to personally submit the remaining documents (confirmation from the broker, application and form 2-NDFL) to the tax service, or send them by mail.

STEP 5: WAIT FOR MONEY

The tax service checks the declarations and accompanying documents confirming the correctness of the calculations and the validity of the requested deduction within 3 months from the date of their submission to the tax authority. Upon completion of the audit, the amount of overpaid tax will be credited to the bank account whose details the owner of the IIS indicated in his application.

This article will be of interest to those who are interested in investing their money, as well as how to receive money from the state. Of course, we have not forgotten about the accounting employees of banks, brokerage companies and other financial organizations, who are tax agents when calculating personal income tax and deductions for transactions subject to accounting on IIS.

What is an individual investment account

First, let us clarify that an individual investment account (IIA) is an account designed for separate accounting of funds and securities of a client - an individual. Such an account is opened and maintained in accordance with Art. 10.2.-1 Federal Law of April 22, 1996 N 39-FZ “On the Securities Market”.According to the agreement for maintaining an IIS, the client is allowed to transfer only funds, with the exception of cases when funds are transferred to the IIS from another IIS.

In this case, the total amount of funds that can be transferred during a calendar year under such an agreement cannot exceed 1,000,000 rubles.

An individual has the right to have only one agreement for maintaining an individual investment system.

There are some restrictions on transactions reflected in the IIS. For example, it is not allowed to purchase federal loan bonds intended for the population using IIS - OFZ-n (53001RMFS). Transactions carried out as part of the activities of a forex dealer are also not allowed.

Investment deductions

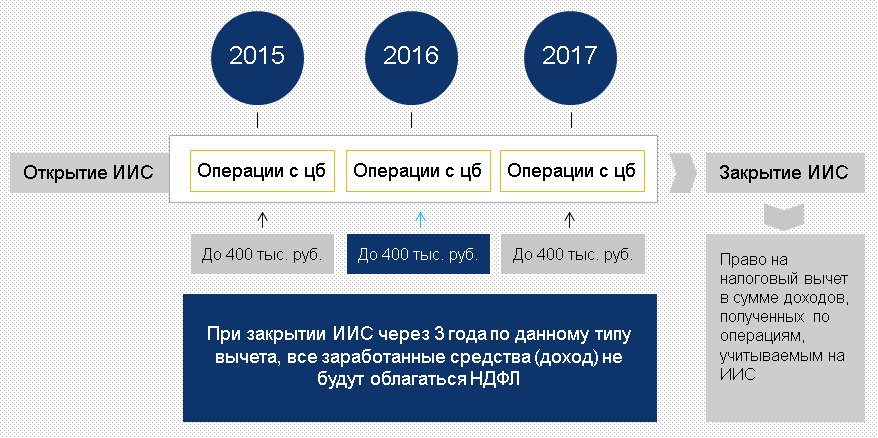

The Tax Code of the Russian Federation provides for three types of investment deductions. For operations on IIS, two of them are provided (optional):For the amount of funds deposited into the IIS, but not more than 400,000 rubles. (the deduction limit in the amount of 400,000 rubles remained, despite the increase in the size of the permissible contribution to IIS to 1 million rubles);

The amount of positive financial results obtained from transactions recorded on the IIS.

1. Deduction for the amount of funds deposited into the IIS

In this case, the amount of personal income tax refundable for the year can be 52,000 rubles, if at least 400,000 rubles are deposited into the IIS. and if the taxpayer’s annual income, taxed at a rate of 13%, was at least 400,000 rubles.

If the contract for maintaining an IIS was valid for less than three years, then the individual must restore the amount of personal income tax for previous years that was not paid in connection with the use of the deduction and pay it to the budget along with penalties.

The deduction can be claimed annually during the term of the contract for maintaining an IIS, provided that funds are replenished in the IIS. The profitability from operations on an IIS account does not matter.

Receiving a deduction is possible based on the results of the calendar year from the tax authority by providing:

- tax return in form 3-NDFL;

- agreement with a broker (trustee);

- documents confirming the transfer of funds to the IIS.

To receive investment deductions, the IIS must be valid for at least 3 years.2. Deduction for the amount of positive financial results obtained from transactions accounted for on the IIS

The maximum amount of deduction is not limited. The deduction can be used upon expiration of the contract for maintaining an IIS (at least three years!). You can choose to receive a deduction in one of the following ways:

- from the tax agent on the date of closure of the IIS, submitting, along with the corresponding application, a certificate from the tax authority stating that this IIS is the only one, and no deduction was provided for the amount of investments in the IIS. The tax agent will reduce the tax base from transactions on IIS by the amount of the deduction.

- at the tax authority by submitting a tax return in form 3-NDFL at the end of the year.

Pay attention to this feature regarding income in the form of bond coupons. If the coupon is included in the sales price (revenue), then such income is taken into account when calculating the investment deduction. If the coupon was received from the issuer during the period of ownership of the bond, then such income is not income from sales and is not included in the calculation of the investment deduction (Letter of the Ministry of Finance dated August 29, 2017 N 03-04-06/55349).

Tax base calculation

The procedure for calculating the tax base for transactions accounted for on an IIS is similar to the procedure for calculating the tax base for transactions accounted for in regular brokerage accounts. The main feature is that the tax base is calculated separately from other brokerage accounts.Let us recall that the tax base for transactions with securities and for transactions with derivative funds is determined in accordance with Article 214.1 of the Tax Code of the Russian Federation. The specifics of determining the tax base for transactions reflected on the IIS are established in Art. 214.9 Tax Code of the Russian Federation. The financial result (tax base) is defined as the sum of financial results for sets of transactions. The Tax Code of the Russian Federation identifies, in particular, the following sets of operations:

1) with securities traded on the securities market;

2) with securities not traded on the securities market;

3) with derivatives trading on the organized market;

4) with derivatives that are not traded on the organized market.

The financial result for transactions accounted for on the IIS is determined by summing up:

Financial results determined for the relevant transactions at the end of each tax period of the agreement for maintaining IIS,

The financial result determined as of the date of termination of the specified agreement.

The procedure for offsetting losses between sets of transactions:

Tax base that can be reduced by loss | Type of loss |

For transactions with derivatives traded on an organized market, if their underlying assets are securities, stock indices or other financial instruments (stock derivatives) | |

For transactions with securities traded on the Ordinary Securities Market | For transactions with derivatives traded on the organized market, if their underlying assets are securities, stock indices or other financial instruments (after reducing the tax base for transactions with all derivatives traded on the organized market) |

For transactions with all derivatives traded on the organized market | For transactions with derivatives traded on an organized market, if their underlying assets Not are securities, stock indices or other financial instruments ( Non-fund derivatives) |

Result from transactions with securities | Result from transactions with derivatives | Balancing result |

||

Stock | Non-stock |

|||

| Certificate in form 2-NDFL, including: | ||||

| Σ = (1) + (2) + (3) | ||||

| 2-NDFL: Σ = (1) - [(2) - (3)] (if Σ>0) | ||||

| or: | ||||

| Certificate of losses: Σ = (1) - [(2) - (3)] (if Σ<0) | ||||

| 2-NDFL: Σ = (1) + [(3) - (2)] | ||||

| 2-NDFL: Σ = (1) + [(2) - (3)] | ||||

| 2-NDFL: (1) | ||||

| And | ||||

| Certificate of loss: Σ = [(3) - (2)] | ||||

| Certificate of losses: (3) | ||||

| 2-NDFL: Σ = (1) - (2) (if Σ>0) | ||||

| or: | ||||

| Certificate of losses: (3) + [(2) - (1)] (if (2) > (1)) | ||||

| 2-NDFL: (3) + [(2) - (1)] | ||||

| 2-NDFL: (3) | ||||

| Certificate of losses: (1) Σ = [(2) - (1)] | ||||

| Certificate of loss: (1), [(2) - (3)] | ||||

| 2-NDFL: [(3) - (2)] | ||||

| And | ||||

| Certificate of losses: (1) | ||||

| Certificate of losses: (1), [(3) - (2)] | ||||

| 2-NDFL: Σ = [(2) - (3)] - (1) (if Σ>0) | ||||

| or: | ||||

| Certificate of losses: (1) Σ = [(2) - (3)] - (1) (if Σ<0) | ||||

| Certificate of loss: (1), [(2) + (3)] | ||||

The amounts of losses received by an individual on transactions with instruments not traded on the securities market do not reduce the tax base of the current tax period.

Amounts of loss that remained unaccounted for on the expiration date of the IIS agreement are not taken into account when determining the tax base, i.e. such losses can never be offset.

Calculation, withholding and payment to the budget of the amount of tax in relation to income from transactions accounted for on the IIS are carried out by the tax agent in the following cases:

1) on the date of payment of income to the taxpayer (including in kind) not on the taxpayer’s IIS - based on the amount of the payment made (for example, when a coupon, partial repayment or dividends on securities accounted for on the IIS are credited to a brokerage account);

2) on the date of termination of the contract for maintaining an IIS, with the exception of the case of transfer of all assets accounted for in an IIS to another IIS opened to the same individual.

The tax agent is obliged to pay the calculated amount of tax to the budget no later than one month from the date of payment of income or the date of termination of the contract.

When terminating the agreement for maintaining an IIS, the tax agent determines the tax base separately for each tax period in which the agreement for opening and maintaining an IIS was in force.

Transactions with currency, transactions in currency

The exchange rate difference itself does not generate income subject to personal income tax. At the same time, when calculating the tax base for transactions carried out in foreign currency, the following should be taken into account.

Income (expenses accepted for deduction in accordance with Articles 214.1, 214.3, 214.4, 214.5, 218 - 221 of the Tax Code of the Russian Federation) of the taxpayer, expressed in foreign currency, are recalculated into rubles at the official rate of the Bank of Russia established on the date of actual receipt of the specified income (date of actual expenses).

When determining the tax base for transactions with securities denominated in foreign currency, the financial result is determined by converting into rubles:

Amounts received from the sale of securities, at the Bank of Russia exchange rate effective on the date of actual receipt of income from the sale of securities,

Amounts paid for their acquisition, at the Bank of Russia exchange rate valid on the date of actual expenditure on their acquisition.

As for REPO transactions, income/expense on such transactions is recognized as interest received/paid. The date of receipt of income (incurrence of expenses) under a REPO transaction is the date of actual fulfillment (termination) of the participants’ obligations under the second part of the REPO. At this moment, the Bank of Russia rate is determined for converting income/expenses into rubles.

If there are no rubles on IIS

The tax agent is obliged to withhold the calculated amount of tax from ruble funds taxpayer at the disposal of the tax agent, based on the balance of the client’s ruble funds in the relevant accounts formed on the date of tax withholding.Withholding the amount of tax in relation to the tax base determined by the tax agent for transactions not accounted for on the IIS from the taxpayer’s funds placed on the IIS is not allowed.

The withholding of tax amounts from the taxpayer's funds in foreign currency, as well as the forced conversion of funds in foreign currency into rubles, are not provided for in Article 226.1 of the Tax Code of the Russian Federation. At the same time, the taxpayer can give an order to convert funds in foreign currency into rubles and be credited to the appropriate accounts opened with the Bank.

If there are no rubles in the account or there are not enough rubles to withhold the tax, then the tax agent sends a message about the impossibility of withholding the tax amount to the tax authorities before March 1 of the year following the expired tax period. In this case, the tax is paid by the taxpayer in accordance with Article 228 of the Tax Code of the Russian Federation, namely:

- no later than December 1 of the year following the expired tax period, on the basis of a tax payment notice sent by the tax authority,

- in relation to income, information about which was submitted by tax agents to the tax authorities for 2016 - no later than December 1, 2018 on the basis of a tax payment notice sent by the tax authority.

The volume of funds in individual investment accounts (IIA) in Russia has grown almost 2.5 times. In Russia, as of mid-December 2016, more than 177 thousand IIS were opened. If the amount of assets in IIS accounts at the end of 2015 was just over 5 billion rubles, then by the end of this year this volume may already exceed 12 billion. The influx of money into IIS is increased due to annual bonuses, bonuses and 13 salaries.

What are the benefits of opening such an account in terms of taxes?

The owner of the IIS receives a tax deduction from the state. You are given one of two tax deduction options, which in different forms can compensate for the 13% income tax (personal income tax). That is, in three years, when investing each year a maximum amount of 400 thousand rubles, you can get 156 thousand rubles - and this is only due to tax benefits, without taking into account the result from the investments themselves.Another option is when the investor does not take advantage of the contribution benefit, but all income received from operations on the IIS is exempt from paying personal income tax after three years of the account’s validity.

At the end of 2016, there has been an increase in the influx of funds into individual investment accounts - in particular, these are those bonuses, bonuses and 13th salaries that in past years people transferred to deposits without unnecessary hesitation. It is also worth taking into account the desire of investors to receive a more substantial amount of tax deduction next year, because for this it is necessary to have time to purchase assets before the end of the current year.

What is the best way to manage the funds in an individual investment account?

IIS owners choose strategies for themselves depending on their level of experience and knowledge. For those new to the financial market, it is usually recommended to use conservative solutions. For example, bonds of reliable companies. Some new clients buy dollars and euros at favorable exchange rates. Some choose riskier strategies. Those who already have successful experience investing in the market, for the most part choose aggressive strategies and actively trade shares in the derivatives market.Is it possible to return personal income tax without unnecessary hassle and going to the tax authorities?

There are fewer and fewer formal obstacles to opening an individual investment account. There are services, including those from investment companies, that allow the account owner to easily receive a completed Form 3 of personal income tax for submission to the tax authority.IIS is gradually becoming one of the drivers of development of the domestic stock market. The innovation increases people's interest in investing, because thanks to tax incentives there is an opportunity to try their hand at the stock market. Government support already suggests that this market is an important part of the economy and personal financial planning. The growing popularity of IIS is accompanied by such factors as a decrease in rates on bank deposits and an increase in the financial literacy of the population.

What if step by step? What are the instructions for opening an investment account and returning personal income tax?

- Where to come?

To a licensed brokerage or management company. - What documents should I have with me?

To open an account, it is enough to have a Russian passport. - What paperwork do I need to fill out?

Standard kit for opening a brokerage account. Our employee will prepare all the necessary documents for the client. - How long does it take to open an account?

No more than 20 minutes. - Do I need to already decide on an investment option before coming to the office?

The client can make a fundamental decision on investment, as well as on what strategy will be used, both when opening an individual investment account and later.

Can you describe in detail the options for returning personal income tax if you open an individual investment account?

1 option— annual 13% discount on contribution. Open an IIS and deposit up to 400,000 rubles into it. This contribution reduces the tax base: the investor can count on a personal income tax return from the budget in the amount of up to 13% of the amount deposited into the IIS. That is, by opening an account for a maximum of 400,000 rubles, you can count on a personal income tax refund of up to 52,000 rubles. To do this, you need to contact the tax service with a certificate from a broker, which indicates the amount of funds deposited into the IIS.At the end of tax season, any refund due will be deposited into your bank account. If the investor adds funds every year, then the operation can be repeated annually - deposit funds into an IIS and reduce the tax base by 13%. An important point: such a tax refund can only be received by an investor who has already paid personal income tax (for example, from salary) during the year when the contribution was made. Therefore, the investor can expect a refund of no more than the amount of tax already paid to the treasury. When closing an investment account, you will have to pay a 13% tax on income received from transactions in the account.

This option may be suitable for conservative investors: 52 thousand with a contribution of 400 thousand per year is practically “in your pocket”, and this profitability can be increased with the help of conservative investments.

Option 2— Income without tax. This type of individual investment accounts assumes that the investor does not receive a contribution benefit, but all income received from operations on the IIA is exempt from personal income tax after three years when closing the IIA.

This option may be of interest to active traders who are willing to accept higher risks in anticipation of potentially higher returns.

When choosing the type of individual investment account, it is worth remembering that although you cannot change the type of IRA, you do not make the choice for life. After three years, you can close the account and open a new one - with a different type of taxation.

You have opened an IIS. Already deposited funds into your account. Bought stocks or bonds. And your money is already working and making a profit. It's time to get your tax deduction. How to do it?

In this article we will analyze a step-by-step algorithm for obtaining a tax deduction on an investment account. What, where and how needs to be done in order to receive the legally due 13% of the amount of funds deposited into the IIS.

So, let's go.

In short, the entire mechanism can be described in just a few steps.

- Collection of necessary certificates and documents.

- Filling out a declaration in form 3-NDFL.

- Providing a package of documents according to paragraphs 1-2 to the tax office.

- Receiving the money.

Let's start in order.

When to submit a declaration?

Upon expiration of the reporting period. In simple words, next year. That is, the tax deduction for 2018 can be received starting from 2019.

One important point. You can get your money back only within 3 years. For example, for 2018 you can receive tax deductions in 2019-2021. In 2022, the right to receive money for 2018 expires.

You can exercise the right to deduct at a time for previous years. If you have never filed returns during these periods. For example, if you opened an IIS in 2015. In 2018, we fill out three separate documents 3-NDFL for 2015-2017.

The maximum refund amount directly depends on the amount of taxes withheld from you to the budget. You will not be able to get back more than you paid.

Step 1. Collecting documents

What documents will be needed?

Certificate of income and taxes paid on it in form 2-NDFL. We receive it at the place of work. If you changed your place of work during the year or have several sources of income, then you need (but not necessarily) to take several certificates.

Do not forget that you can return only 13% of the amount deposited. In some cases, a certificate from only one place of work will be sufficient.

Example. Over the past year, 200 thousand rubles were deposited into IIS. From this amount you can return 13% or 26 thousand rubles. During the year you changed your job. Do you need 2 certificates or is only one enough?

We look (remember, find out) how much you earned during the year both here and there. We roughly multiply this amount by 13%. And if you are confined to one place of work, then there is no point in submitting a second 2-NDFL certificate to the tax office.

Let's say at your previous job you received 40 thousand a month. We worked for six months. About 30 thousand were paid in taxes.

You only managed to work at your current job for 3 months with a salary of 50 thousand. Withheld taxes amount to about 20 thousand.

In this case, it is better to take one certificate of income from your first place of work.

Agreement with a broker on opening an individual investment account (copy). Provides only the first time. No need for next years.

Documents confirming the fact of crediting funds to the IIS. This can be a payment order (for bank transfers) or a cash receipt order (for cash deposits).

The easiest way is to print out all the movement of money from the personal account of the bank from which you carried out transactions. No seals or signatures of bank employees are needed.

Here's what it looks like in my example:

All details are provided. Just like there is a mark on the bank’s execution of your order. This is quite enough for the tax office.

Broker's report on the movement of funds and securities in the account. We order directly from the broker. Needed for tax purposes to show the availability of money in an individual account. After all, it was possible to deposit money and then safely withdraw it at the end of the year. And claim a tax deduction.

Application for refund. Indicating the bank details of the account where you want to receive the money. A sample is available at any tax office.

Step 2. Filling out the declaration

The documents have been collected. It's time to start filling out the declaration.

There are 2 options here:

- fill it out yourself and for free;

- pay and they will do everything for you (or almost everything).

The paid service for filling out the 3-NDFL declaration costs from several hundred to several thousand. It all depends on the appetite and impudence of the “offices”.

Some people, most likely out of ignorance or because of fear of the unknown and possible difficulties in filling out, pay money for the service.

The procedure for filling it out yourself does not cause any difficulties. And it won't take much time. Literally half an hour. Well, a maximum of an hour - for the “not the fastest”))).

Should I order a declaration for money or not?

There is an expression: Saving means earning.

How much does the service cost? For example, 600 rubles. Imagine that in half an hour you can earn 600 rubles. Not in a mine, not carrying bags of flour, but just sitting at home at the computer. Would you agree to such a part-time job? I would definitely agree.

Moreover, when ordering paid services, you will still lose time. While you are being consulted. Additionally, you will need to provide the necessary package of documents to fill out (scans or photos). Passport details, TIN, income certificate, movement of funds, etc., etc.

As an example, I will give a price list for the services of one popular service.

In general, it is much faster and more profitable to do everything yourself.

So, let's fill out the declaration.

First, you need to download a small program tailored for the declarations of individuals.

Let's create a new document. And fill in all the required fields.

Setting conditions.

By default, this tab contains everything as it should be. But better check. It should look like the picture below.

Pay attention to the “Adjustment number” field. Initially you need to set zero. During the audit of your return, the tax office may find filling errors. In this case, when editing and correcting these comments, you will need to enter the correction number - “1”.

By the way, the program automatically checks that the fields are filled out correctly and warns the taxpayer every time about possible errors when switching between tabs.

In the previous screenshot, I did not fill in the “Inspection Number” field. Switching to another window, the system displayed the following message.

You will find the inspection number in the program directory. Enter your region number and then select from the list provided.

Tab "Information about the declarant".

Everything is elementary and intuitive - and there is nothing to add on my own. Fill in “Personal Data” and “Address”

Many people have difficulty with the OKTMO field. What kind of animal is this? And where to find these “magic numbers”?

OKTMO is an all-Russian classifier of municipal territories.

But that doesn't matter to us. The main thing is where to find out the required code.

Information about OKTMO is in the 2-NDFL certificate provided to you by your employer.

Tab “Income received in the Russian Federation”.

For individuals, taxes paid at a rate of 13%, select tab 13. Click " green plus " - "Sources of payments." And we enter information about the employer. We take information from the 2-NDFL certificate.

Accordingly, if there are several sources of income. Fill in several fields.

Information about income. Again we take all the data from the 2-NDFL certificate. And we drive everything one into one.

Pay attention to the income code.

In 99% of cases, you will have the following code in the help:

- 2000 - receiving wages (usually a salary);

- 2002 - bonus from the employer;

- 2012 - vacation pay.

Therefore, in one calendar month there can be 3 sources of income.

After filling out all income for the employer, we compare the total amounts in the declaration with the paper certificate 2-NDFL for errors. The amounts must add up to kopecks.

I remember several years ago, when filling out my first declaration for a property deduction, I made a mistake of just a few kopecks. After 3 months I received a notification from the tax office. I had to correct and submit the declaration a second time (remember? correction number 1). The tax authorities checked the second version of my return for almost 3 more months. And it took a month for the money to reach the account after verification.

As a result, this whole procedure dragged on for almost 7 months (instead of the standard 4). For a few extra pennies.

Therefore, it is better to waste a little time and check everything thoroughly: every ruble and penny.

The last tab is “Deductions”.

In theory, we need to immediately go to “Investment and losses on the Central Bank”.

But I would like to draw your attention to the “Standard” tab. If you skip filling out this sheet, the tax office may reject your return in the future.

Standard tax deductions are . By default, you receive this money at work (if you provide the necessary certificates to the accounting department). More precisely, less taxes are withheld from you. The amount of the required deductions.

You must enter information depending on your position.

If there are no children. You can safely skip this field.

The last push. Tab " Deductions" — -> Investment and losses on the Central Bank.

In the field: “Amount of deduction provided for in paragraph 2, paragraph 1 of Art. 219.1 of the Tax Code of the Russian Federation" - we write the amount you contributed to the IIS for the reporting period.

That's all. The declaration is completed. All that remains is to check for errors. If everything is fine, the “Declaration verification completed successfully” window will appear.

We save it to our computer. Will be needed for the future. If adjustments need to be made. Or next year. It will only be enough to edit the income and the amount of funds deposited into the investment account.

Step 3. Interaction with the tax office

Personal visit or the old-fashioned way. Take the entire package of documents, print out the declaration and go to the tax office. Just like at a bank, we take an electronic queue coupon to the required window.

As a rule, the whole process happens quite quickly. Even despite the presence of people. In the last few years, standing in line literally takes 10-15 minutes.

We give all the papers to the inspector. That's all. Let's move on to the next step.

Important! In the 3-NDFL declaration, you need to put a signature and date on each sheet. The date is not the time of preparation, but of submission to the tax office. Therefore, it is better not to register dates in advance, but directly to the inspection. Otherwise, you will simply be “turned back with the old dates.”

Step 4. Pleasant - receiving money

The declaration has been submitted. All that remains is to wait.

According to the law, the maximum period for verification is 3 months from the date of filing the declaration. And 30 days to transfer money to the bank account specified in the application.

Nothing depends on you here.

But there are some tips from an “experienced” person.

When submitting a declaration at the beginning of the year (January-early February), verification in 95% of cases occurs much faster. Literally 1-1.5 months. For a friend of mine, the entire cycle from filing a declaration to receiving money in his account took 3 weeks.

This is due to the “low workload” of tax office workers at the beginning of the year. Few taxpayers rush to submit their returns immediately after the New Year holidays. It takes several months for them to get going. And the bulk of the documents “fall in” in March - April - May. And here you will almost always have to wait for the maximum specified period.

The problem is a little different. Usually, the employer cannot provide a 2-NDFL certificate immediately after the New Year. And a little later. It's the same with the broker. When ordering a certificate, the standard waiting period is several weeks. And not right away either. And usually after a month and a half from the beginning of the year.

As you can see, there is nothing complicated. Having gone through such a cycle once, you don’t understand why you should pay extra money for filling out the 3-NDFL declaration.

You can even speed up the entire process of preparing, filling out and submitting a tax return. If you use the site itself. On which it is possible to perform all the above procedures without leaving home. Up to filing a declaration without a personal visit to the inspection. But more about this in.