Accounting in 1s. Accounting info. Balance sheet and profit and loss statement of the enterprise

Every organization immediately after its creation is required to keep accounting records. According to the law of December 6, 2011 No. 402-FZ, accounting and storage of documents is organized by the head of the LLC. The director is responsible for organizing accounting in the organization, and even financial statements are recognized as drawn up after the signature of the director, and not the chief accountant. Entrepreneurs are luckier in this sense - it is not required by law.

Accounting is the organization of collecting information about the state of the property and obligations of the company, as well as the continuous reflection of this information in special accounting documents. But LLC accounting is not only registers, accounting books and financial statements. These are also tax accounting documents, contracts, personnel and primary documentation, documents on cash flow (cash and bank). We have collected the entire extensive list of documents that need to be maintained in an LLC in the article "".

Please note: for violation of accounting rules. Accounting support services are not something you should save on, especially since they will not require any special expenses.

Is it difficult to keep books for an LLC? The answer to this question will depend on several factors:

- Selected tax regime. It is enough to simply keep records on the simplified tax system Income and UTII. It’s more difficult - using the simplified tax system Income minus expenses. The most difficult thing will be accounting for the general taxation system.

- Availability of employees. Reporting for employees is complex and voluminous; in addition, it is necessary to prepare salary calculations and payment of insurance premiums every month, and, if necessary, also vacation pay, sick leave, and maternity payments. But even if there are no employees, and the only founder runs the organization without an employment contract, it is necessary to submit zero reports. In addition, all organizations, even those without employees, must annually submit information about. And new organizations must submit it no later than the 20th day of the month following the month of registration.

- Number of operations. These are any business actions that have changed the ratio of income and expenses of the organization: receipt of payment from customers, payment of wages, purchase of goods, etc. The more transactions there are, the longer it will take to complete them.

- Diversity of activities of the organization. There are specific accounting features in certain areas of business (trade, production, services, construction, etc.). It is easier to account for operations of the same type than to combine accounting for different areas.

- Category of your partners. If you and your counterparty work under different tax regimes, if you plan to conduct foreign economic transactions or work with budgetary or state-owned enterprises, then the accounting will have its own peculiarities.

But even in the simplest version - the absence of employees, a small number of operations, choosing the simplified tax system Income or UTII mode - accounting for an LLC will require professional knowledge or the use of specialized programs. Accounting services for an LLC can be entrusted to a full-time employee or a specialized company. - this is a complete or partial transfer of accounting responsibilities to a professional independent contractor.

Accounting statements of LLC

Accounting in an LLC must ensure the completeness of collection and recording of information about the financial activities of the organization. Where to start with LLC accounting?

Step 1. Determine who is responsible for maintaining accounting records at the enterprise. Often, after registering a company, the director assigns the responsibilities of the LLC accountant to himself. At first, this is a completely acceptable situation, but as soon as the deadline for submitting any reports approaches, you need to either figure out this issue yourself or transfer the service to specialists.

Step 2. Choose you will work. This must be done immediately after registering the LLC, or better yet, before you submit the documents to the Federal Tax Service. When choosing a regime, we recommend that you receive a free tax consultation, which will help you save significantly on payments in your budgets. Under different regimes, the tax burden of the same enterprise can differ significantly!

Step 3. Review your regime's tax records. On the simplified tax system you need to submit only one declaration at the end of the year, on UTII, quarterly declarations, on OSNO, every quarter you submit declarations on profit and VAT and an annual declaration on property tax.

Step 4. Develop and approve organizations.

Step 5. Approve the working chart of accounts. The document should be based on the chart of accounts developed by order of the Ministry of Finance of Russia dated October 31, 2000 N 94n.

Step 6. Organize accounting of primary documents and reflection of the information contained in them in accounting registers.

Step 7 Comply with the chosen tax system and reporting for employees.

Our users can receive a free month of accounting services provided by 1C:BO specialists with the transfer of the 1C Accounting information base after the end of the trial period.

Law No. 402-FZ includes a balance sheet, a statement of financial results and appendices to them as the financial statements of an LLC: reports on changes in capital; cash flow; on the intended use of the funds received (if they were received).

Balance sheet and profit and loss statement of the enterprise

The forms of the enterprise’s balance sheet and LLC’s profit and loss statement were approved by Order of the Ministry of Finance dated July 2, 2010 No. 66n. Later, by order of the Ministry of Finance of Russia dated 04/06/2015 No. 57n, the profit and loss statement was renamed to the financial performance statement. Organizations are required to submit financial statements at the end of the year no later than March 31 of the following year. But investors, creditors, banks, and counterparties have the right to request a report on financial results during the year, so you can make a snapshot of the financial condition of the LLC based on the results of the quarter or month.

The LLC balance sheet form can be found in appendix. No. 1 to Order of the Ministry of Finance of July 2, 2010 No. 66n. This is the so-called full balance on two pages.

Accounting statements of an LLC using the simplified tax system in 2019

How to keep accounting records for an LLC under the simplified tax system Income 6% and under the simplified tax system Income minus expenses? The simplified taxation system involves submitting just one annual tax return. Its shape is the same for both versions of the simplified system.

What financial statements do LLCs submit to the simplified tax system in 2019? Keeping accounting records under a simplified taxation system allows you to submit financial statements in a simplified form (Appendix 5 to Order of the Ministry of Finance dated July 2, 2010 No. 66n). It includes only the balance sheet and income statement. If the organization received targeted funds through the simplified tax system, then they also need to be reported. It is not necessary to submit reports on changes in capital and cash flows.

An example of filling out a simplified balance sheet of an LLC using the simplified tax system:

Accountant services for LLC

Let's summarize. Accounting services for LLCs are mandatory in all tax regimes and even in the absence of real activity of the company. Bookkeeping can be done by the manager himself, a full-time specialist, or a specialized outsourcing company. for an LLC will depend on the volume of work: the number of business transactions, the complexity of the chosen mode, the number of employees, and the method of accounting.

For our users who want to do their own accounting for an LLC, we want to offer the 1C Entrepreneur online program. This is a completely new tool for increasing business efficiency, which allows you to:

- maintain full accounting and tax records;

- carry out settlements with counterparties;

- issue and pay invoices and payment orders;

- calculate any payments to employees;

- save all LLC documents in a single database;

- analyze sales, income and expenses;

- choose the minimum possible tax burden, etc.

For a long time, no one has been doing accounting manually. Special programs are used for accounting at enterprises. The company 1C has gained wide popularity in this field, producing many standard solutions aimed at performing various accounting tasks of an enterprise.

In this article we will talk about one of the most common configurations of 1C Accounting, namely 1C version 8.2. The 1C 8.2 program consists of a platform and configuration: the platform has different versions (for the purposes of this article, platform version 8.2 is considered) and the Accounting configuration.

1C:Enterprise 8 and 1C:Accounting 2.0

Accounting 8.2 is used for maintaining automated accounting and tax accounting at enterprises of various forms of ownership, including the preparation of regulated reporting in accordance with the requirements of the legislation of the Russian Federation.

Accounting 8.2 has several editions. For platform version 8.2, the configuration with revision number 2.0* is used. There was an even earlier edition of Accounting 1.6 and a later edition of 1C Accounting - 3.0. Edition 3.0 is used with the more modern platform version 8.3. To switch to version 3.0, you will also need to update the platform. Because This article is devoted to the 8.2 platform, then we will talk about what capabilities Accounting 8.2 in version 2.0 has.

*Edition is an update of the 1C configuration, which is associated with the improvement of the system in technological and functional terms, due to new legal requirements, the development of IT technologies or the emergence of new business methods.

Accounting 8 contains all the reference books necessary for an accountant’s work: documents, reports, and also allows you to collect reports without any extra effort, which optimizes and at the same time simplifies the work of an accountant. At the same time, version 8.2 allows you to keep records simultaneously for several organizations.

Features of accounting in version 8.2

Accounting for several organizations in one database

Unlike version 7, in 1C: Accounting 8 accounting has become more convenient due to the fact that accounting for different organizations can be kept in one database using common directories, which certainly simplifies the process* when enterprises are interconnected. Thanks to this feature, 1C: Accounting 8, namely the version under review - 8.2, is in demand both in small enterprises and in holdings.

*This function is useful not only for accountants, but also for business managers, since they can receive reports for all organizations at once from one database.

Accounting for different taxation systems

1C:Accounting 8.2 allows you to keep records for organizations with different taxation regimes:

- General taxation regime. Version 2.0 uses a unified chart of accounts for accounting and tax accounting*;

- Simplified taxation system (STS). Provision is made for keeping records of income and expenses;

- Unified tax on imputed income (UTII). Allows you to maintain separate income and expenses for the activities of the enterprise under the general regime and those falling under UTII.

When using version 8.2, there is no need to purchase several configurations for accounting for organizations and individual entrepreneurs that use special modes.

*In version 1.6, two separate charts of accounts were used for accounting and tax accounting.

Customization options

Let's look at the main features that are available in Accounting 8.2 and distinguish it from other versions and editions.

To simplify work in 1C: Accounting 8 there are various assistants:

Launched when the program is opened, it helps to facilitate filling out and checking the basic program settings, directories, and entering initial balances. Also, using this assistant, you can transfer data from previous versions of 1C.

Often accountants are faced with a problem when they need to make a certain entry, but they do not know which document should be used to reflect this in the 1C system. For this purpose, in version 8.2 a new assistant has appeared, called the “Invoice Correspondence Directory”. In addition, this guide will help you find out which document to use to reflect the necessary posting, where to find it in the program and what type of operation to choose.

Accountants who are just getting used to the 1C Accounting program will especially appreciate such an assistant. This assistant is located in the Operations – Account Correspondence section.

The assistant looks like this:

This assistant is designed to simplify work when entering data about new employees in 1C, calculating salaries and taxes on them. The assistant is located in the Salary section - Payroll Assistant.

Changes in the chart of accounts and reflection of transactions in version 8.2

1C: Accounting 8 includes a chart of accounts approved by order of the Ministry of Finance of the Russian Federation. Users can now add new accounts, new subaccounts, and analytical accounting sections independently. To maintain tax accounting, a unified chart of accounts is used, and the sign of maintaining tax accounting is set in the chart of accounts in the “Tax” attribute.

The settings of each account can be seen by opening the account by double clicking the mouse:

Accounting in Accounting 8.2 is carried out “from the document” - this means that documents reflecting a business transaction are entered into the program, and when carried out, the document generates transactions and entries in registers. Tax accounting is carried out automatically when documents are reflected in 1C. One transaction now reflects data on both accounting and tax accounting. You can view the transactions and entries in the registers that were generated by a specific document by clicking the “Result of document posting” button.

The screenshot shows that accounting and tax accounting data are in one entry, the amounts are indicated in different columns.

In the Accounting 8.2 program, most business operations are automated. However, in practice, it happens that an accountant is faced with the need to reflect a non-standard transaction, for which a separate document is not provided in 1C Accounting. To do this, the program has manual data entry, where the posting is directly entered. The previous version of the program required the entry of two documents. One document was used to enter accounting entries, and another document was used to make entries in registers*. In the version under review, this work is simplified due to the fact that now entering transactions and data into registers is carried out in one document, which is called “Operations entered manually.”

*For this purpose, the document “Adjusting register entries” was used.

Procedure for closing a period

When closing a period, many routine operations are performed in a strictly defined sequence. The program for closing a period has an assistant called “Closing the Month”. You can find it in Operations – Processing – Month Closing. Before closing, the document entry sequence is checked in chronological order to detect documents that may have been entered backdated, which could lead to accounting errors. To restore the sequence, you must use the “Repost Documents” button. After completion, sequence control will be restored and it will be possible to begin closing the period. If the accountant is sure that the documents entered retroactively will not lead to accounting errors, then you can not repost the documents, but click the “Change key date” button, thereby recognizing the existing sequence of documents as correct.

In version 8.2. edition 2.0, when closing a period, you can clearly see which operation was carried out successfully, in which errors occurred, and which operation was not carried out at all. For clarity, everything is highlighted in a different color.

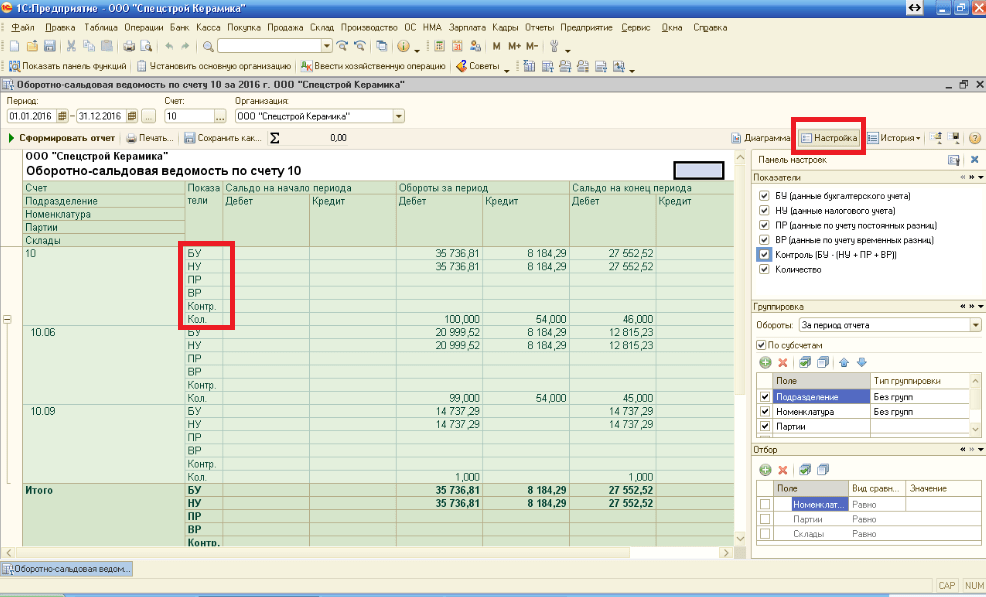

You can use reports to reconcile, compare and organize data. In version 8.2, reconciliation of data between accounting and tax accounting has become more convenient, since the version of the program discussed in this article allows you to see them in one report. New opportunities have appeared in reports for grouping, sorting, customizing and selecting data.

For example, we will use the “Account balance sheet” report. When setting up a report, you can use the settings panel (opened by clicking the “settings” button on the right side of the report) to display in the report the necessary data on tax accounting and control of accounting equality with tax accounting.

We looked at the basic functionality and some features of the Accounting 8.2 program in edition 2.0, which make it possible to simplify and improve accounting at any enterprise, but this is far from an exhaustive list of all the program’s capabilities.

MINISTRY OF EDUCATION AND SCIENCE OF THE RF

SIBERIAN FEDERAL UNIVERSITY

KHAKASS TECHNICAL INSTITUTE – BRANCH

Federal State Autonomous Educational Institution of Higher Professional Education "SIBERIAN FEDERAL UNIVERSITY"

A.V. Ivashina

I.A. Smirnova

Basics of work in 1c: Accounting 8

Tutorial

UDC 657.1.011.56

Reviewers:

A.S. Dulesov, Doctor of Technical Sciences, Head. Department of Information Technologies and Systems, Khakass State University. N.F. Katanova;

E.A. Balabanova, Candidate of Economic Sciences, leading specialist of the State Committee on Tariffs and Energy of the Republic of Khakassia.

Basics of work in 1C: Accounting 8: Textbook on the discipline “Subject-oriented economic information systems” for students of specialty 080801.65 – Applied informatics (in economics) full-time and part-time courses for laboratory work / Comp. A.V. Ivashina, I.A. Smirnova: Krasnoyarsk, Siberian Federal University, 2010. 222 p.

Printed by decision

Editorial and Publishing Council of the University

UDC 657.1.011.56

© KhTI – branch of Siberian Federal University, 2010

INTRODUCTION 5

Chapter 1. Basic concepts of accounting 5

1.1. Subject, method and objectives of accounting 5

1.2. Basic accounting rules 6

1.3. Active accounts 9

1.4. Passive accounts 10

Chapter 2. Basic concepts 1C: enterprises 8.1 10

Chapter 3. Accounting in the 1C: Accounting program version 8.1 18

3.1 Starting the program 18

3.2Creating a new user 26

3.3 Preparation of the information base 31

3.4Starting assistant 38

3.5 Charts of accounts 50

3.6 Entering initial balances 56

3.5 Methods of registering business transactions 60

3.5 Cash accounting 67

3.7 Accounting for fixed assets 79

3.8 Materials accounting 109

3.9 Accounting for goods and services 120

3.10 Accounting for production, release, sales of finished products 149

3.11 Personnel and wages accounting 175

3.12 Settlements with accountable persons 197

3.13 Accounting for intangible assets 205

3.14 Peculiarities of accounting for VAT and corporate income tax 212

3.15Reporting system in 1C: Accounting 8.1 217

3.16 Regulatory operations and formation of financial results at the end of the reporting period 224

CONCLUSION 227

LITERATURE 228

1. Alexandrova, E. I. 1C: Accounting 8.1 from scratch! [Text] / E. I. Alexandrova, M. K. Beilin. - Best books, 2010, 272 p. 228

5. Kharitonov, S.A. 1C: Accounting 8 for beginners [Text] / S.A. Kharitonov. – Peter, 1C: Publishing, 2009, 384 p. 228

Introduction

The purpose of this course is to study the theoretical foundations of accounting in the 1C:Enterprise 8.1 program, as well as to obtain practical skills in working with the 1C:Enterprise 8.1 program.

In the application solution 1C:Accounting 8, enterprises with various types of activities can keep records: wholesale or retail trade, commission trade, provision of services, production or construction.

In one information base you can keep records of the activities of several organizations and individual entrepreneurs. In this case, general directories of counterparties, employees and items are used, and reporting is generated separately.

The program supports various taxation systems: general regime, simplified tax system and UTII.

1C:Accounting 8 stores complete information about counterparties (contact information, bank accounts, registration codes) and employees of the organization (passport details, individual codes, position, salary).

1C:Accounting 8 automatically generates various forms of accounting and tax reporting, which can be printed or saved to a file for transmission to the Federal Tax Service.

This manual consists of three parts. The first part deals with general accounting issues. The second part presents the basics of the 1C: Enterprise system, the third part directly describes the issues of reflecting basic business transactions in accounting.

An essential feature of 1C Accounting 8.2 is the parallel maintenance of accounting and tax accounting.

1C Accounting edition 2.0 simultaneously and simultaneously maintains accounting (BU) and tax (TA) accounting for calculating income tax.

According to our Tax Code, it turns out that in order to calculate income tax, you need to maintain.

In simple situations, accounting and tax accounting may completely coincide; accountants often deliberately combine accounting and tax accounting. But situations often arise when such a combination is impossible: excess of normalized expenses, differences in the timing of acceptance of income and expenses, partial or complete non-acceptance of expenses in tax accounting. In such cases, permanent and temporary differences arise, which must also be taken into account.

In any case, when the accounting policy of an organization in 1C Accounting 8.2 states that the enterprise pays income tax, the 1C Accounting program automatically conducts double calculations: accounting and tax calculations for profits. If all operations in the program are formed correctly, then it is possible to fill out an organization’s income tax return (in the regulated reports section) and automatically fill out a large number of profit tax accounting registers (the “Reports” menu).

To correctly understand the methodology for tax calculations on profits, a good understanding of the relevant chapter of the Tax Code on profits and knowledge of PBU 18/02 is required. All NU mechanisms in 1C are built on the basis of these documents.

1C Accounting 8.1 (revision 1.6) maintained two charts of accounts: “self-accounting” for accounting and “tax” for tax accounting of profits. When posting documents, they generated postings simultaneously according to two charts of accounts. And there were two groups of reports: on the self-supporting chart of accounts and similar reports on the tax chart of accounts.

In 1C Accounting 8.2 (revision 2.0), the principle of tax accounting has changed. There was only one chart of accounts left - the self-accounting one, but it now became possible to simultaneously carry out accounting and tax accounting documents. And the reporting functionality has changed. Now in the settings of all standard reports there are BU indicators for displaying accounting data and NU, PR, VR for displaying tax accounting in the report.

This approach slightly complicated the appearance and settings of reports 8.2, but on the other hand, it has now become convenient to compare BU and NU data in one report at once. In addition, in 8.2 it has become easier to fill in the details of primary documents when filling out; now you do not need to separately enter accounts and subaccounts for tax accounting.

To see how accounting and accounting entries are generated using accounting documents 8.2, you need to open the document entries ( Dt/Kt button in the document toolbar) and in the document posting result form, enable the “show/hide NU data” button. Then columns for tax accounting will appear in the transaction lines: NU (tax accounting), PR (permanent differences) and TP (temporary differences) in separate cells, as shown in the image (picture clickable).

Conclusion: Accounting 8.2 (version 2.0 configuration) simultaneously maintains accounting and tax accounting in 1C on one chart of accounts, and the report settings have indicators for displaying BU, NU, BP and PR data.

Postings of accounting and tax accounting in 1C Accounting 8.2

1. Regularly create copies of infobases

1C specialists talk about this all the time, everyone knows this rule, but, unfortunately, not everyone follows it. It’s a pity if you have to remember the obligation to regularly copy the 1C database based on your own bitter experience. Believe me, those clients who have restored their accounting at least once after losing their database will forever remember how important this rule is.

In what cases can database copies help you:

- physical breakdown of the computer/server;

- virus infections;

- damage to the 1C information base itself;

- “unexpected” changes in data in the information base (if you suddenly discover that for some reason the data from previous periods has changed, it is possible to restore a copy and compare the information, find the reasons for the discrepancies).

You can create copies in different ways: upload manually (I described in detail how to do this in the article “Creating a copy of the database - why is it needed and how to do it”) or use special programs for automatic copying. But in this case, you must remember that in order to protect the database from viruses and physical damage to the computer, you need to store copies of the database on some other media, for example, connect an external drive or flash drive, unload the database and disconnect the drive. However, it is very inconvenient to act this way every day, so the best option is to connect the 1C: Cloud Archive service. In this case, copies of your database will be created automatically and stored outside your local network - in the cloud. In the event of a breakdown or virus infection, you can restore copies from another computer at any time and start working. If you want to find out details about connecting this service, which is also part of the comprehensive contract for support of 1C: ITS, then fill out the application form, we will definitely call you back and tell you everything in detail.

2. Set a date for banning editing

After you have submitted your reports, you must close the period for editing to prevent accidental changes to the data. In 1C: Enterprise Accounting 8 edition 3.0, for this you need to go to the “Administration” tab and select “Support and Maintenance”.

Then expand the “Routine Operations” item, put a tick next to the date of prohibition of changes and click on the “Configure” link.

We indicate the date – the last day of the closing period.

3. Close documents with a cross

Acquire a useful habit - closing documents with a cross if you opened them just to look. Very often I come across a situation where an accountant generates an OCB, expands to the account card to find out detailed information, opens the necessary document to look at it, and then closes it by clicking the “Post and Close” or “OK” button. In this case, the document is reposted, the amounts in the postings may change, and the sequence of document posting is confused. And then, at the close of the next month, the accountant is in for a surprise - in September the program “wants” to repost all the documents from January or even from last year. To prevent this from happening, it is necessary to set a date for prohibiting editing and not to repost documents unnecessarily, but simply close them with a “cross”.

4. Do not rename directory elements and carefully change their settings

Why can’t this be done or must it be done very carefully? It is necessary to understand that the changes made will affect the entire period of accounting in the program. For example, if you change the name of the counterparty, then the new name will be displayed in all printed forms, including earlier documents. To prevent this from happening, in 1C: Enterprise Accounting 8 edition 3.0, to change the name there is a special “History” link, where you can indicate from what date the new value is valid.

You also need to remember that, for example, changing the settings of the “Cost Items” and “Other Income and Expenses” directories may lead to changes in financial results after the month is closed and data in regulated reports. I talked about one similar situation that happened with my clients in the article “Why can the data in the reports of closed periods change? "

5. Regularly update information databases and analyze changes

Updates for 1C programs are currently released quite often, and they need to be installed sequentially, so it is imperative to keep your databases up to date in order to avoid emergency situations during the reporting period. After all, it may turn out that you urgently need a new reporting form, which are released with enviable regularity, and the neglected situation with updates can greatly fray your nerves. If you work in 1C via the Internet or you have a support agreement with our partners, you will not need to worry about this issue. If you update your databases yourself, then please pay due attention to this serious issue.

It will also be useful to take an interest in the results of the past update, because new functions are constantly appearing in the program and operating algorithms are changing. To keep abreast of all events, you can go to the “Administration” tab, select “Support and Maintenance”.

6. Do not duplicate entries in directories, use the 1C: Counterparty service

It happens that, having not found some counterparty in the directory, users add a new one, although in fact the required counterparty has already been entered into the database, but with some errors in the name, TIN or necessary fields are simply not filled in. It also happens that counterparties double-check when downloading bank statements for the same reasons. In this case, problems begin with the offset of advances, the balance of accounts 60 and 62 varies, problems arise with calculating VAT on advances and paying expenses to get into the KUDiR under the simplified tax system. In order to prevent such situations, I recommend using the 1C: Counterparty service, which will automatically fill in all the necessary information correctly, and regularly monitor the order in your directories.

7. Do not number documents and reference books manually

The program provides certain algorithms for automatic document numbering. If you decide to interfere with them, correct some number, for example, by adding a slash or some other symbols to it, then be prepared for the fact that in the future you will also have to monitor the numbering manually.

8. Enable display of accounting accounts in settings

By default, in the 1C: Enterprise Accounting 8 edition 3.0 program, the display of accounting accounts in documents is disabled. But I believe that an accountant is obliged to “keep his finger on the pulse” and constantly monitor the correctness of entering primary documents, without trusting the program to completely fill out such important details as accounting accounts. Therefore, we make sure to enable the display of accounting accounts in documents and make sure that materials are received on account 10, and not on account 41. To do this, go to the “Main” tab, “Personal settings” item.

Check the box “Show accounting accounts in documents.”

9. Correctly use subaccounts for 60 accounts

I have already spoken many times about how important it is to correctly use the advance accounts - 60.02 and 62.02, and how important it is to control the status of mutual settlements on the 60 accounts. Now I have decided to make this point a separate rule, which also must be observed. You should not argue with the program, trying to impose on it your opinion that the account data is not needed; you will still lose in this dispute, receiving in return a mess in your accounting.

I discussed this question in detail in one of my video tutorials. “How to bring order to account 60 in 1C programs”

10. Do not change the chart of accounts yourself

If you decide to add your accounts to the chart of accounts, you need to be prepared for the fact that this will entail certain difficulties. For example, once they approached me with the following problem: “We decided to put things in order in the accounting of fixed assets and added subaccounts to account 01 in accordance with the fixed assets groups, after which depreciation stopped accruing.” When adding subaccounts to account 20, there may be problems with closing the month, and subaccounts to a number of other accounts will not be included in the balance sheet - assets and liabilities will not match.

Very often, the issue can be resolved in another way without changing the chart of accounts, and if this is still required, then it is necessary to seek the help of specialists who could assess the consequences and make the necessary changes, ensuring the correct operation of the program.

I also discussed this question in detail in my article. “Adding your accounts and subaccounts - is it necessary to do this and what the consequences may be.”

11. Minimize manual entries and adjustments

I always encourage people to avoid manual operations and document movement adjustments as much as possible. Currently, accounting in 1C: Accounting 8 is automated quite well and the need for manual entries does not arise so often.

The fact is that it is not always possible to make the entries correctly on your own; for example, the picture below shows an attempt to close advances to a supplier using a manual operation, but the third subconto (“Settlement Documents”) is not filled out. Such an adjustment can only aggravate the situation with mutual settlements, and in no way solve it.

I also published a detailed article on this topic, which I highly recommend reading: “Manual wiring - why doesn’t 8 “like” them? »

12. Correctly reverse documents

In order to reverse document movements, you need to create a special operation with the “Document Reversal” type.

In no case should you simply generate transactions manually, because in addition to entries in accounting accounts, the program reflects information in various registers necessary, for example, for calculating VAT. If you do not reverse the entire document, but correct something manually, then corrections also need to be made for all other registers.

Prompt receipt of information from regulatory authorities about changes in report statuses and received requests- without leaving the program, it is possible to quickly see changes in the status of the report, quickly find out about its acceptance or return with errors, it is also possible to receive requests from regulatory authorities and immediately respond to them.

You can always easily find the latest version of the report, which was actually sent - this is a very important point! After all, there are situations when, in attempts to finally collect information into a final report, several copies of one form are created, the data is changed, saved, and then it is very difficult to find the version that was actually sent. And this becomes especially relevant if it is necessary to prepare a corrective document. It takes a long time and tediously to verify information manually, wasting precious minutes of working time. If you send reports directly from 1C, next to the desired option it will be indicated that the report has been submitted; a long search will not be required.

Let's be friends in